Tool -

Tool -

Water-related financial disclosures fall within the broader concept of sustainability reporting, which is the disclosure and communication of environmental, social, and governance (ESG) goals—as well as a company’s progress towards them. The aim of reporting ESG is to help companies to better measure and manage their exposures to ESG-related risks and to become better corporate citizens by measuring, disclosing, and managing the environmental and social impacts they create (EY - Oxford Analytica, 2021).

Sustainability reporting is based on the concept of materiality. A material sustainability issue is an economic, environmental, or social issue on which a company has an impact or may be impacted by (NYU-Stern, 2019). Materiality analysis is the process through which a company systematically identifies, selects, prioritises, and reviews what is material to the company and its stakeholders, and thus merits inclusion in sustainability reports (Calabrese et al, 2019).

The issue of water scarcity is generally considered to be a material issue for major beverage and food companies (e.g., PepsiCo, Coca-Cola, Heineken, Danone, etc.). These companies rely on water to produce its products, and without a consistent supply of inexpensive water, would likely face significant business challenges. Because other people rely on the same water resources, the companies may face pressure from stakeholder groups who object to its sourcing of water from communities in water-stressed regions. Thus, water-related risks become a material issue for corporate players (Tool C5.05) creating an incentive to disclose water-related financial information.

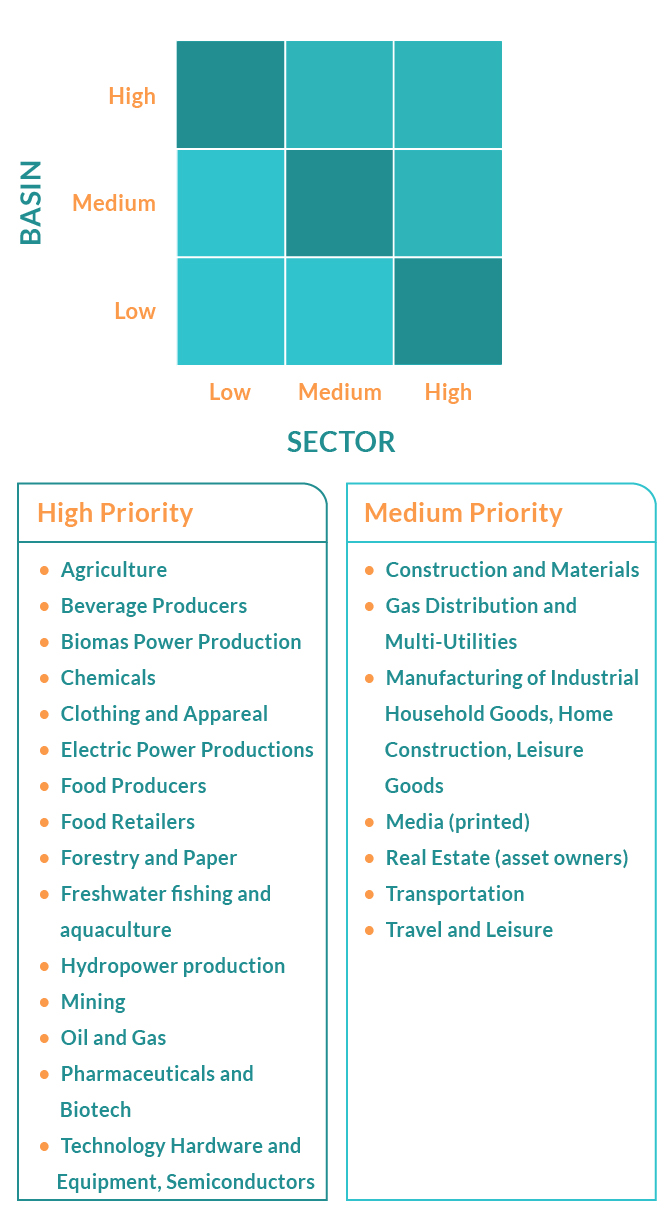

Water-related financial disclosures are especially beneficial to companies in sectors that have high exposure to water-related risks. These are generally but not exclusively water-intensive industries businesses (Figure 1). Companies that use little water can also have a high exposure to water risks (e.g. for instance technology companies that use water in only some key aspects of their operations). Sector-specific risks vary however based on the basin in which these industries operate (Figure 1). Those in the red and orange categories in Figure 1 will find sustainability reporting for water most beneficial.

Figure 1. Measures of Exposure to Water-Related Risks (Adapted from )CEO Water Mandate, 2014.