Tool -

Tool -

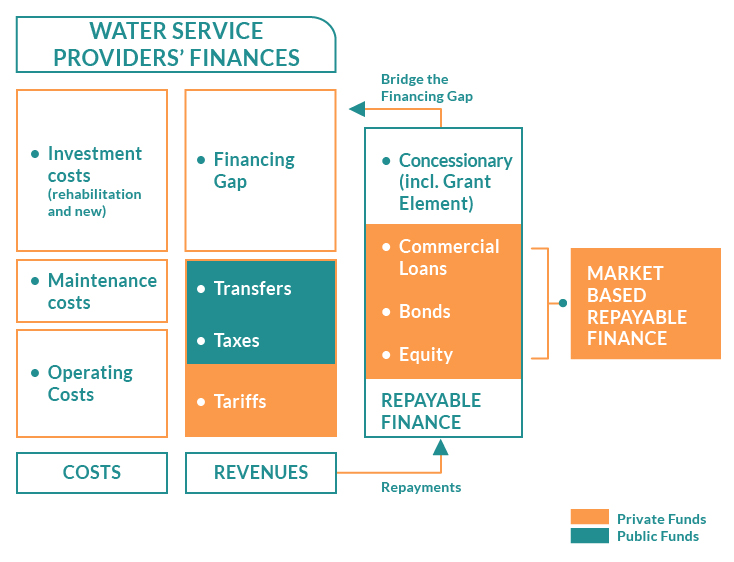

Private or public water and sanitation service providers need financial resources to make infrastructure investments with high upfront costs and to operate and maintain them. This means utilities need to leverage investment capital and working capital through loans, bonds, and/or equity, known as repayable finance mechanisms (Figure 1). The main source of capital are development banks (national or international), financial institutions (such as commercial banks), and institutional investors (sovereign wealth funds, insurers, pension funds, private equity funds, endowment funds, among others). International development banks, such as World Bank, Interamerican Development Bank, African Development Bank, Asian Development Bank, and European Bank for Reconstruction and Development played a key role in promoting private participation in water provision.

Figure 1. How Repayable Finance Works (Adapted from OECD, 2010).

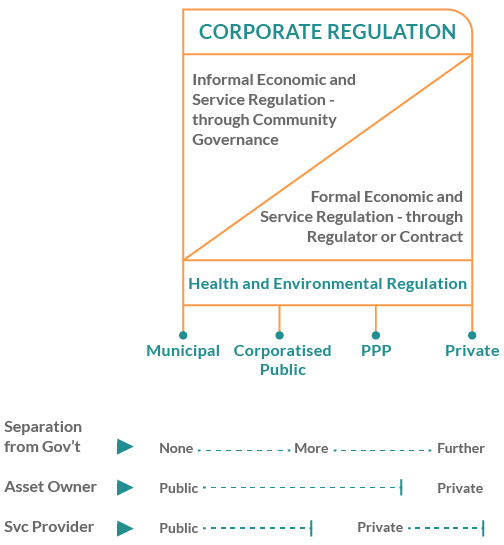

Water service providers can be either public or private companies depending on institutional arrangement society has agreed on and the values it has decided to pursue to achieve a desired social outcome. Rouse (2013) identifies four business models: municipal, corporatised public, private-public partnerships (PPP), and private. They differ in terms of “the degree of separation from government, asset ownership, and whether the [provider] is public or private” (Rouse, 2013; see Figure 2). This classification is not broad enough to include community-based organisations, that is, when communities organise to provide water themselves without the intervention of government (Bakker, 2010). Under Rouse’s parameters of classification, the latter are fully private, however, ownership is collective.

Figure 2. Main Business Models for Water Service Providers (Adapted from Rouse, 2013).

Each of these business models has specific features that make them more or less attractive for investors. For example, the public and corporatised models are more suitable for indirect investments such as loans or bonds. Governments may take credits directly from development banks or commercial banks on behalf of the public agency in charge of supplying WASH. Corporatised public utilities may also issue bonds and back them with a “sovereign guarantee” (a financial clause by which the national government assumes the service of debt in the case of default). On the other hand, PPPs and private utilities are more interesting for private financiers. The former is a hybrid in which assets ownership is retained by the state (local, regional, or national governments) while management is transferred to a private provider that has as a main driver is to profit from operating water infrastructure (Marin, 2015). Both PPP and private utilities may also be recipients of loans and bonds and, in some cases, they might also issue equity through a public offering, in the local stock exchange, or privately, for specific investors.

A key aspect to attract financing sources for any of these types of service provider is “creditworthiness”. This is a measure of a borrower’s ability and willingness to service its debt obligations. To be creditworthy, a utility must demonstrate a reliable stream of positive cash flow from operations as well as sufficient cash reserves in the case that future cash flows are not sufficient. The degree of creditworthiness is judged through a valuation performed by lenders or independent parties to determine the borrower’s potential for defaulting on its debt obligations. There are various tools available for assessing credit, from creditworthiness indexing to shadow ratings to credit ratings (World Bank, 2017).