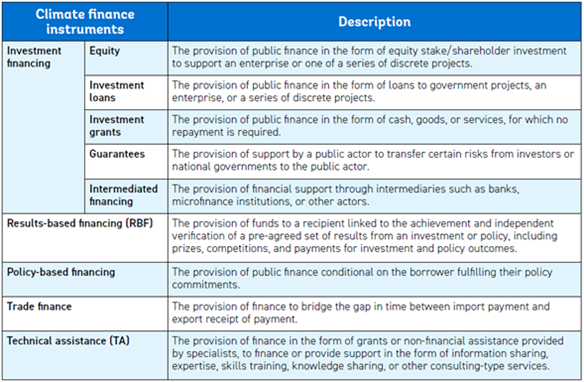

The water and climate sector uses the same financial structures (project finance, public-private partnerships) and instruments (loans, guarantees, bonds, insurance, equity) that any other industry. However, there are some financial structures that work better for water and climate resilient projects (Table 1).

Table 1. Summary of Climate Finance Instruments. Source: World Bank (2020).

Moreover, the last decade has witnessed the emergence of innovative financial structures which are being piloted and can be replicated and scaled-up at a global level. Here are some of the most innovative financial structures in the market (N.B. this is a selection rather and an exhaustive taxonomy of these sort of financial instruments).

- Green debt: It takes the legal form of a traditional lending product, where a private or public borrower obtains credit from a bank in return of a financial commitment (interest rate) to use the proceeds to finance projects or assets that deliver environmental outcomes (mitigation and/or adaptation goals). Depending on the borrower’s size and risk profile, these loans are syndicated by lenders and have shorter maturity than in the case of other financing instruments such as green bonds. The difference between traditional loans and green debt is that the latter have become more attractive, as the introduction of new technologies for water and waste water treatment might reduce significantly operation and maintenance costs and increase revenue generation, which downplays the risk of default. Moreover, there is a special structure called “Sustainability-Linked Loans”, defined as loans provided by lenders in return for sustainability commitments assumed by the private borrowers and agreed between borrowers and lenders that, if accomplished, might result in interest-rate reductions (Deutz et al., 2020).

- Green Bonds: They are debt instruments issued by either public or private organisations to raise capital in the domestic and international capital markets (public offering) or placed privately with a limited number of investors (not listed on a public exchange). Investors receive full repayment of the bond issuance amount (the “principal”) in addition to interest payments on outstanding principal amounts (the “coupon payments”). Green bonds are similar to ordinary bonds except that investment proceeds are restricted to finance green projects and assets. The determination of whether a bond is actually “green” is left to issuers and investors (For a taxonomy of water projects that can apply to green bonds financing, see table 2). The water sector accounted for 8% of the total climate-aligned bonds (US $101 billion) or 10.1 % of the green bonds in 2018, with proceeds used for improving the climate resilience of water assets (Deutz et al., 2020)

Table 2. Green Bonds Taxonomy for the Water Sector Projects. Source: Climate Bonds Initiative (2021).

- Results-based financing: This structure is “a financing modality or approach under which a donor or investor (also known as “principal”) disburses funds to a recipient (also known as “agent”) upon the achievement and independent verification of a pre-agreed set of results” (World Bank, 2017). In the water sector one of the innovative experiences of the use of results-based financing is wastewater treatment in Brazil with PRODES (River Basin Clean-up Programme in English), established in 2001 by the National Water Agency. This programme aimed to reduce water pollution in watersheds by giving financial subsidies to public investors based on pollution targets (reduction in discharge of untreated sewage, that is, “payment for results”) instead of giving financial support to projects while they were built (“paying for the work”). Since it was created, a total of 80 wastewater treatment facilities were constructed through this programme, benefitting about 9M people. Approximately US $118 million has been disbursed in subsidies and the equivalent to US $468 million has been leveraged in total investments (ANA, 2016).

- Environmental Impact Bonds: This a financial instrument through which a beneficiary party (or outcome payor), often a governmental entity, enters into a contractual relationship with a group of risk investors to procure a needed service or intervention on a pay-for-success basis. The outcome payor benefits from the fact that it is not required to repay the investors unless predetermined metrics (which indicate the service or intervention has been successful) are achieved. Given the conditionality of the returns, it is in the investors’ interest that competent service providers are hired and that these service providers deliver strong results that satisfy the predetermined metrics (Deutz et al., 2020). The first bond of this class was issued in 2016 by the District of Columbia Water and Sewer Authority (USA) to control storm water runoff in excess due to increasing urbanisation (conversion of natural landscapes into housing projects) and changes in precipitations due to climate change. The proceeds have been used to construct green infrastructure practices designed to mimic natural processes to absorb and slow surges of storm water during periods of heavy rainfall, ultimately reducing the incidence and volume of combined sewer overflows that pollute the District’s waterways. If the predetermined runoff control thresholds are achieved in excess, investors will get a performance payment of US $3.3 million; if the solutions perform as expected, investor will not get any premium and are paid at a market rate; however, if those solutions underperform, investors will pay the District of Columbia Water and Sewer Authority a US $3.3 million risk share payment (DC Water, n.d.).

- Green Insurance and Catastrophe Bonds: The insurance industry offers to different products that fits the objective of adaptation in the water sector. Based on the model of a parametric insurance, defined as “an agreement to make a payment upon the occurrence of a triggering event” (Swiss Re, 2018), a Catastrophe Bonds (CAT) is a financial instrument by which “the holder (i.e., the beneficiary) of the policy receives a pay-out when a disaster reaches a predetermined threshold, and investors lose part, or all, of the principal that they have invested. If no disaster exceeds the threshold that triggers a pay-out, the investor receives the promised interest on his investment and the principal is returned at the close of the coverage period” (Cooley et al., 2020). An example of this instrument is Jamaica’s CAT that will provide the government with financial protection of up to $185 million against losses of three Atlantic tropical cyclone seasons ending in December 2023 (World Bank, 2021). A special type of CATs is Resilient Bonds, which “links insurance premiums to resilience projects in order to monetise avoided losses through a rebate structure that is used to fund proactive risk reduction projects and reactive disaster recovery actions” (Veolia Institute, 2018). The first Resilient Bond was issued by the European Bank for Reconstruction and Development to use the proceeds to finance existing and new climate resilience projects such as the rehabilitation and modernisation of a 60-year-old hydropower plant in Tajikistan and a water conservation project for an irrigation system in Morocco (EBRD, 2019).

Tool -

Tool -