Tool -

Tool -

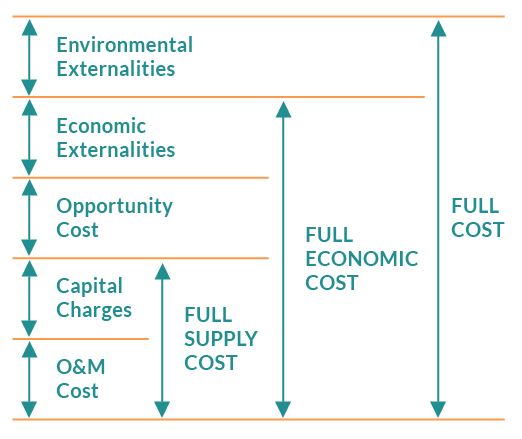

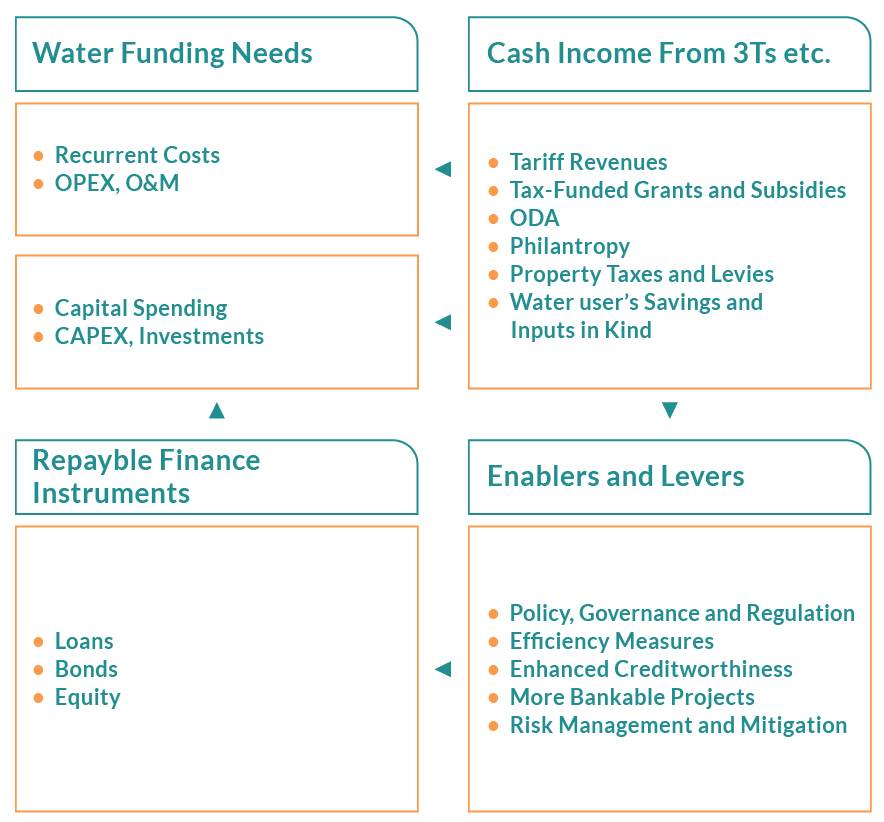

The term “investment” is generally used to describe the economic value creation processes in which productive assets yield benefits over a future period. In the water context, investment therefore also includes the funding and financing perspectives (Fig. 1). Funding corresponds to income or cashflows that water projects generate which mainly comes from “3Ts”, which stands for tariffs, taxes, and transfers (Tool D2.03). Financing, in turn, refers to accessing resources for capital investments and covering operational and maintenance costs which are paid back with funding sources. The choice of funding and the flows of financing depend on political environment, regulation framework, institutional arrangements, as well as conditions of capital markets. Funding and financing are mutually dependent when efficient finance reduces the funding requirement for water-related projects, and credible funding streams help secure low-cost finance (WWC and GWP, 2018).

Figure 1. Sources of funding and financing (Adapted from SWA, 2020).

The cost of this investment needs to be funded in various ways through private and public funds or a mixture of both – charging water users, investments from government budgets, and external aid. Most of the water infrastructure investment traditionally comes from the public domain. However, in recent times, there is a growing involvement of private commercial entities in sharing these costs (e.g., using water tariffs to protect watersheds through investment vehicles such as water funds).